Insights

Branch of the Future in the Banking Industry

April 15, 2021

Mass adoption of new technology has changed customer behavior and expectations in the banking industry over the last few decades. Where physical branches and call centers were once consumers’ only touchpoints with their bank, today’s customers have come to expect a certain level of digital experience. More than 50% of consumers now want an omnichannel banking experience, where they can interact with banks at their convenience.

With increasing market competition, the otherwise content Canadian customer has also become less tolerant of bad customer experiences, including slow fulfillment and long approval times. Industry research shows that nearly 70% of customers who plan to leave their bank attribute their decision to poor service quality rather than poor products.

On the other hand, the evolution of bank branches has been relatively slow, and most branch-level processes have stagnated since the 20th century. Branches continue to have only a transactional focus on customer interactions, and a considerable portion of back-office fulfillment processes are still either entirely or largely manual. Reliance on expensive human capital is an obstacle to process efficiency and cost reduction, and the bottlenecks it creates can hinder customer experience.

The Need for Branch Transformation

In many ways, the current situation creates an ideal path forward, where both customers and banks want to move to a new and improved banking experience. The Branch of the Future should allow banks to transition from the current slow, expensive, and sometimes frustrating branch experience to something faster, cheaper, and better while keeping the personal touch that makes branches so resilient.

There is a significant overlap between the expectations of consumers and banks from branch transformation. Both, for instance, want the Branch of the Future to enable personal, interactive customer service in an omnichannel manner. Branch transformation should also improve customer service turnaround (reduce time-to-decision and time-to-fulfillment) and create a holistic sales focus rather than a transactional focus.

Additionally, banks may want to reduce branch space and staffing levels and entice customers to move to more profitable service channels without increasing churn. For customers, this will translate into lower service costs and a wider pool of engagement channels for their financial services needs.

By stepping into the future with an ecosystem of intelligent, digital technologies, banks can maximize revenue while driving a holistic sales focus emphasizing customer-centricity and client-driven innovation.

What Should the Branch of the Future Look Like?

Before banks can embark on this transformation journey, it will be essential to define what the Branch of the Future looks like and what functions it needs to deliver. Only once banks have a clear picture of their expected future state can they start defining a transformation roadmap.

Keeping in mind the goals of both consumers and banks, there are several things the Branch of the Future should offer. These include:

Virtual Branch

Customer expectations and requirements from financial institutions have changed significantly in the last few years. The shift of digital engagement channels has happened at an unprecedented pace, accelerated lately by the pandemic. Also, changing customer demographics have prompted banks to re-evaluate their customer service channels and enable a holistic omnichannel experience. However, most online channels, such as websites or apps, are devoid of the personal touch that customers have come to expect from their banks.

This gap between convenience and customer-centricity can be bridged by creating a virtual branch. A virtual reality-based simulated environment can imitate actual branch premises, allowing customers to interact with bank employees and products/services in the same manner as they would in a real branch, but from the comfort of their homes. To make customer interaction more convenient, virtual branches can be made available 24/7, overcoming staffing limitations through offshore recruitment.

Zelusit’s Virtual Branch opens unique opportunities for product and service presentation and brand representation and can take customer interactions to a whole new level. Our solution will allow your bank to simulate traditional 1:1 meetings with virtual, private meeting features, digital presentation capabilities, and built-in document verification and signature tools for easy onboarding. Customers can expect the same level of personalized attention they would receive in-branch via virtual guides, live chat, and voice communication features.

The Virtual Branch platform has built-in customer journey analytics capabilities and diligently tracks and analyzes data from customer interactions to provide in-depth insight into customer behavior, preferences, and product sales. The solution integrates seamlessly with CRM systems to facilitate lead and account management and can be embedded into your website as a one-stop-shop for all your customer needs.

Brand Representation Quality Assurance

Regardless of any other customer engagement channels banks may add, it is clear that the physical branches are not going away anytime in the foreseeable future. Improving the quality of service in brick-and-mortar locations should remain a key priority for banks, even as they look to expand their digital footprint.

Leveraging a combination of audio and video recognition, AI and analytics, Brand Representation Quality Assurance can deliver intelligent insights to improve customer service, optimize operations, and detect anomalous behavior. Some key areas of improvement could include:

Premises and Interaction Analysis: Today, the branch is the only banking channel that lacks a consistent feedback loop between experience and training. In contrast, telephone banking analyzes all calls and uses the results for agent training, and online banking analyzes clicks and the overall customer journey to improve the website and app interfaces. By ensuring proper brand representation and customer service quality, organizations can continue to deliver on and improve standards for customer satisfaction and reduce customer churn.

For financial institutions, both the branch premises and employees must appropriately represent the bank’s brand. The employees, for instance, must be neat, polite, efficient, and be able to provide suitable, timely service and help customers with the right product offerings. Also, occurrences of aggressive behavior must be detected early and prevented to ensure that the brand is presented positively.

Zelusit’s solution for Premises and Interaction Analysis leverages a combination of input from branch video monitoring, emotional/facial recognition, audio analysis of conversations, and motion tracking with Transaction and Behavioral analysis in real-time using advanced Machine Learning models. Using this solution, the branch can:

- Track movements and appearance of individuals

- Identify employee or customer sentiment

- Identify adherence to brand practices in sales and service

- Detect and forecast violent or aggressive behavior

These insights essentially create a feedback loop and can be used to train branch staff on etiquette, better customer service practices, and dealing with difficult customers/situations. It can also help track employee performance and identify products/services where additional employee training may be needed.

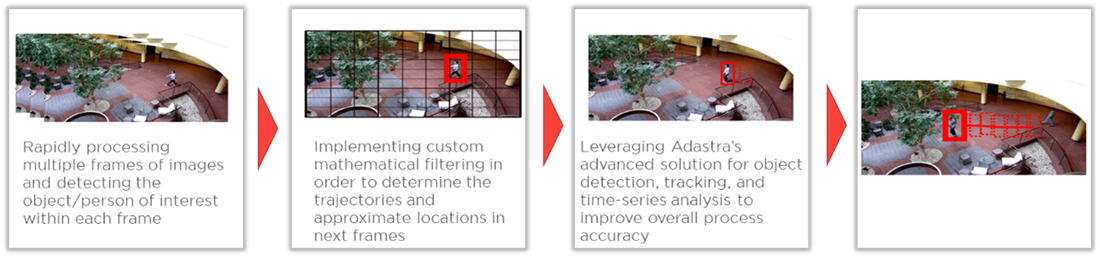

Detecting Lost Customers for Follow Up: During peak hours, it sometimes becomes challenging to keep manual track of branch traffic and ensure all customers receive timely assistance. Currently, for most banks, data on branch traffic is measured by tracking the number of transactions and does not account for “lost” customers or individuals who left without making a transaction, possibly due to a long wait time.

Zelusit’s solution provides real-time insights into branch traffic, allowing the bank to identify “lost” customers or those in need of immediate personal follow up. Using a combination of object detection and tracking models and facial recognition, our solution can track people coming in and out of the branch, flag anomalies, and identify customers for follow up.

By identifying customers who are not adequately served in the branch, banks can ensure outreach through other channels to keep them engaged and satisfied with the customer service.

Operational Efficiency

In most banks, back-office processes are still largely manual, and consequently, approvals and fulfillment are time-consuming exercises. Banks’ heavy reliance on human involvement can be a disadvantage for both overheads and efficiency, and the long wait times adversely impact customer satisfaction. Augmenting back-office and customer-facing fulfillment processes with AI and automation can increase efficiency, reduce costs, and improve overall customer service.

Customer onboarding and document processing are typically the two most time-intensive processes, and Zelusit offers solutions to make them more efficient with digitization and automation.

Digital Onboarding: While a lot has changed in the financial services ecosystem in the last few years, digital customer onboarding is still a pain point for many banks. Due to the documentation, verification, and decisioning processes involved, onboarding is still largely manual and requires significant back and forth between branch staff and customers. Needless to say, for a customer looking to purchase a product/service, facing lengthy processing and wait times is likely not a pleasant experience and does not reflect well on the organization’s brand. This is especially true for younger customer segments, who expect a fully digital banking experience. Moreover, with newer fintech companies starting to offer a seamless digital onboarding capability, banks where onboarding is limited to in-person interactions or where the digital onboarding process is inconvenient may see significant customer churn or lose out on new customer opportunities.

With Zelusit’s Digital Onboarding solution, however, banks can deploy efficient and secure onboarding, covering both front-end and back-end processes. On the customer-facing side, our solution allows organizations to register new clients (or existing clients for new services/products), verify their mobile number using OTP, collect internal and external data on the applicants, including identification documents and photographs, get digital signatures, and showcase product offerings.

In the back-end, the solution has provisions for KYC processing, cleaning and processing images (such as scanned documents), document processing and mining, verifying customer photographs against ID provided, and quick AI-based credit decisioning. The solution can be implemented on both web and mobile interfaces to meet customer needs.

Document Processing and Mining: Manual document processing in the back office takes up to 95% of the sales cycle. Moreover, 30% of branch space is typically dedicated to the storage of paper documents, which has a substantial overhead cost.

Despite the advantages, automating document processing has remained a challenge for most financial institutions. Some of the documents still contain handwritten sections, which makes it hard to use simple OCR tools for document processing. Electronic signature recognition, too, is an obstacle for both front and back-office automation.

Zelusit’s Document Processing and Mining solution can drive efficiency and eliminate the need for expensive human resources and real estate space by consolidating hard-copy information, including, handwriting into an easily accessible database in text form. It can parse through documents in near-real-time, identify key details from elaborate/convoluted documents, and store important information in a searchable format. Also, the solution can validate documentation and provide feedback to branch employees almost immediately, so any errors or gaps can be rectified promptly.

Automated document processing can reduce wait times in customer onboarding and servicing, improve time-to-fulfillment, and consequently, customer satisfaction and retention. Additionally, with less human resources required for back-end documentation, banks can cut costs by reducing branch staffing levels.

Sales Optimization

In an ideal scenario, each banking channel should be optimized to drive sales growth by enabling personalization of product/service offerings based on customer profiles. Most branches, however, continue to have a transactional focus, where customer needs are met as they come up, and there is little room for anticipating customer expectations and tailoring offerings accordingly. Intelligent profiling and AI-powered sales solutions can help banks personalize their products with the objective of exceeding customer expectations.

Customer Segmentation: Accurate segmentation of customers allows organizations to provide them with more relevant product offerings based on their requirements. This goes a long way in improving both conversion rate and customer satisfaction, and consequently, reduces customer churn.

Zelusit’s solution for Customer Segmentation leverages a combination of behavioral and profitability-based segmentation methodologies. It allows for micro-segmentation (based on product use, risk levels, etc.), clustering (based on customer similarities), and profiling (or segment comparison), based on your business needs.

Segmentation is critical for generating customer-centric insights, which can also be used for marketing initiatives, campaigns and promotions, and to enhance loyalty schemes. From a sales standpoint, offering customers a “better fit” product is also more profitable for the organization and strengthens customer relationships and trust in the bank.

AI-Powered Product Sales: AI-based sales solutions can make the customer experience more interactive and intelligently drive sales and cross-selling based on individual customer preferences and transaction history.

Zelusit offers AI-powered Chatbots and Virtual assistant solutions that can be implemented directly in online ads. Customers can interact with the banner ad, which will guide them through a product selection process, offer personalized product offerings, and redirect them to a dedicated landing page on the bank’s website. Chatbots can also be built into banks’ websites and apps to assist customers in their purchase decision-making. Personalized AI advisor bots can also be instituted via video screens to serve as an augmented first line of engagement and reduce unproductive waiting time in branches. The results or advice from these can be linked to a branch employee’s screen as soon as the customer’s turn in line comes up, saving time for both the branch staff and the customers.

These solutions can make customer service more personal and interactive from the get-go, ensure appropriate brand representation, and entice customers to move to more profitable digital channels. For the customer, these intelligent virtual sellers can improve the overall experience and reduce consideration time by offering the most relevant products.

Based on recent customer trends, it is clear that the future of banking is digital, albeit with an emphasis on personalization. However, physical branches will continue to play an important role in the financial services ecosystem for the foreseeable future. Banks will need to find a way to make their branches more customer-focused, effective, and profitable to sustain operations with a dwindling in-person customer base. The ideal Branch of the Future may not look the same for all organizations, and different solutions may need to be implemented to fulfill the goals of specific organizations and their customers. Some of the elements outlined in this article will be foundational to any major digital transformation initiatives at the branch level, while others may be needed as your organization makes progress on its digitization journey.

As a leading data and analytics service provider, Zelusit can help banks design and implement a digital transformation roadmap for their branches. First, our experts will assess your needs, digital maturity level, targeted customer segments, and outline what an ideal Branch of the Future looks like for your organization. Once the target state is clear, we will help you build future-ready, implementable solutions in line with your growth objectives. Our expertise in delivering AI and analytics solutions for the financial services industry leaves us well-positioned to understand industry challenges and create intelligent, customized solutions to address those gaps, so you can continue to offer service excellence to your customers.