Insights

Data Validation, Integration, and Sharing for Climate-Related Financial Risks: Part 2

June 8, 2021

With the recent BCBS and OFSI papers drawing the attention of financial institutions to the measurement of climate-related risks, banks have started evaluating ways in which they can incorporate climate risk data into their risk assessment and business strategy. However, despite the criticality of climate-related analytics, work in this direction has so far remained in the early stages, owing to a lack of clean, complete climate-risk data and uncertainties surrounding the impact of climate change on business and the pace or timeline of climate change.

In the first chapter of this three-part series, we looked at the sources of climate-related data and methods of data collection. Once financial institutions have access to the various sources of climate-related data, be it the National Weather Service, other banks, or data derived from the financial transaction history of their clients and vendors, it becomes important to ensure the validity and veracity of this data, so that it can be used for analytics. Clean, complete data is the foundation of reliable analytics, and in order to extract meaningful, accurate insights, the underlying data must be trusted and mastered. In this chapter, we will focus on data validation, integration, and sharing in a manner that preserves its integrity.

Zelusit’s Data Validation Approach for Climate-Related Data

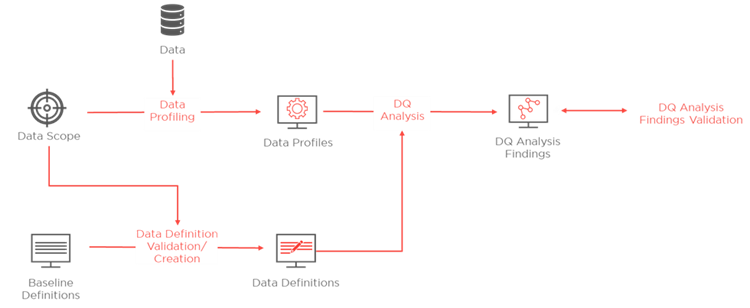

From the perspective of validating the accuracy of climate exposure data, there are two phases of effort we need to look at – initial and ongoing.

In the initial phase, the banks will need to understand the data they are getting from various sources and ensure that they are looking at it consistently. Zelusit proposes an approach involving the following functional components:

- Data profiling

- Data quality analysis

- Extraction of business, technical, and operational metadata

- Creation of a Unified Climate Risk Data Model (UCRDM), representing all the climate risk data based on the sources which a bank receives

- Mapping of data from various sources to UCRDM

A graphical representation of the process is included below:

In reality, many of these activities overlap, but from logical perspective, they can be aligned into 7 steps:

- Identify

- Attributes in scope

- Data lineage

- Entities in an emissions data source

- Attributes in an emissions data source

- Common terms

- Hierarchies

- Relationships

- Data profiles

- Operational metadata

- Understand

- Level of data quality

- Data types

- Business data definitions

- Technical data definition

- Sample values

- Usage

- Equivalence

- Review 1

- Data quality analysis results with business SMEs

- Business metadata with business SMEs

- Technical metadata with technology SMEs

- Define

- UCRDM Subject Areas

- UCRDM Entities

- UCRDM Attributes

- UCRDM Data Types

- UCRDM Entity and Attribute Relationships

- Transformation rules

- Data Quality rules

- Mapping standards

- Map

- Climate risk data source entities and attributes to UCRDM target entities and attributes

- Review 2

- Mapping results with SMEs and Enterprise Architects

- Data model consistency

- Update

- Mapping and model

- Transformation rules

- Create final version

In the ongoing phase, a robust and sustainable governance framework will have to be established around data quality and metadata. The stakeholders of such a framework should include not only internal bank stakeholders, but owners of all emissions data sources and, possibly including other banks, as banks themselves are significant source of emissions data about their clients (as discussed earlier). It stands to reason that such a governance framework can not only take care of data quality and metadata, but also regulate sharing of emissions data between participants, both nationally and internationally.

Establishing a Working Governance and Data Sharing Framework

First, it will involve setting up of an organization which is capable of establishing and maintaining the governance policies, processes, and tools. The organization should also be able to follow the collaborative ecosystem model that many organizations dealing with climate risk, such as PCAF, have pioneered.

Second, such an organization will have to enable the governance ecosystem, i.e., hire or train people, write policies, design processes, select and roll-out data quality and metadata management tools and training for those tools, as well as get buy-in for all of those from the participants.

Then, this organization will need to establish technical standards for data sharing, data quality, and metadata that are neutral, interoperable and royalty free.

And last, but not the least, such an organization in concert with all participants should be able to execute governance processes and use the tools.

Some examples of processes which such a governance organization will need to regulate are processes to support and maintain various governance tools, processes for data quality validations and corrections, metadata management, as well as processes governing data transmission, such as data and API specifications, information security, consent, and data lifecycle (retention, disposal, etc.) processes.

Since we have agreed that banks possess and should exchange their customers’ climate risk exposure data, we should also take into consideration the system of data exchange which needs to be established for this purpose. Realistically, many functions in such a system can be mirrored from Open Banking concepts, provided that we will need specialized APIs covering the scope of exposure data.

With the foundation set with appropriate data collection, sharing, and validation mechanisms, the next step would be for financial institutions to perform analytics to measure climate-related financial risks. Ideally, banks’ focus should be on predicting the probability and net impacts adverse events will have on certain asset classes within a given geography or jurisdiction. In the final chapter of this series, we will discuss some examples of analytics strategies that financial institutions will need to adopt, along with the challenges they will need to overcome.

As a leader in the data and analytics space, Zelusit helps customers appropriately manage their data in a manner that facilitates value extraction. We have over 20+ years of experience in the financial services sector and offer solutions for data management, data governance, master data management, metadata management, and much more, to help banks comply with industry regulation, provide better customer experience, and improve the efficiency of front and back-end processes.